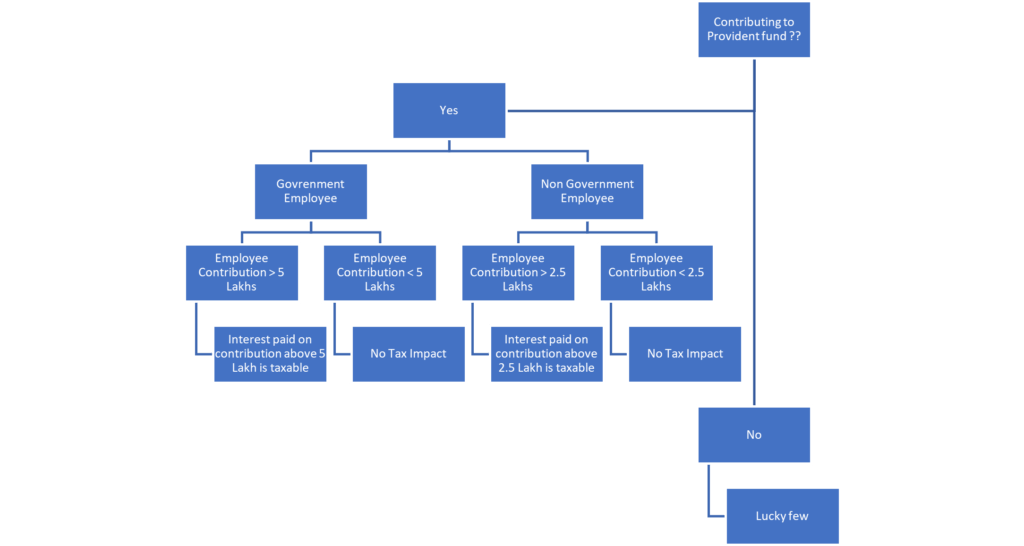

In the Union Budget 2021, Finance Minister Nirmala Sitharaman had announced that the interest earned on employees contributions to their provident fund (EPF) in excess of Rs 2.5 lakh a year will be subject to tax.

The government had then said that the move would affect less than 1 percent of tax-payers. That is, primarily high-earners whose basic annual salary is over Rs 21 lakh (Rs 1,73,612 a month). For government employees, this EPF contribution threshold is higher at Rs 5 lakh. This has come into effect from financial year 2021-22 (assessment year 2022-23).

Employers deduct 12 percent of your basic salary as your contribution to EPF every month, add a matching amount as their contribution and deposit it with the EPFO. If the amount deducted as your contribution is over Rs 2.5 lakh/Rs 5 Lakh (whichever applicable) in a financial year, the interest earned on this excess amount will be taxed as per the slab rate applicable to you. If you have made any additional, voluntary contribution during the year, that will also be taken into account.

Calculation of taxable interest relating to contribution in a provident fund or recognised provided fund, exceeding specified limit.-

For the purpose of calculation of taxable interest, separate accounts within the provident fund account shall be maintained during the previous year 2021-2022 and all subsequent previous years for taxable contribution and non-taxable contribution made by a person.

(a) Non-taxable contribution account shall be the aggregate of the following, namely:-

(i) closing balance in the account as on 31st day of March 2021;

(ii) Contribution made by the person in the account during the previous year 2021-2022 and subsequent previous years upto contribution in excess of 2.5 Lakh or 5 Lakh); and

(iii) interest accrued on sub- clause (i) and sub- clause (ii), as reduced by the withdrawal, if any, from such account;

(b) Taxable contribution account shall be the aggregate of the following, namely:-

(i) contribution made by the person in a previous year in the account during the previous year 2021-2022 and subsequent previous years, which is in excess of the threshold limit (i.e. 2.5 Lakhs or 5 Lakhs); and

(ii) interest accrued on sub- clause (i), as reduced by the withdrawal, if any, from such account;

In view of the impact of the Covid-19 pandemic, taxpayers are facing inconvenience in meeting certain tax compliances and also in filing response to various notices. In order to ease compliances to be made by taxpayers during this difficult time, reliefs are being provided through Notifications nos. 74/2021 & 75/2021 dated 25th June, 2021 Circular no. 12/2021 dated 25th June, 2021. These reliefs are:

Objections to Dispute Resolution Panel (DRP) and Assessing Officer under section 144C of the Income-tax Act, 1961 (hereinafter referred to as “the Act”) for which the last date of filing under that section is 1st June, 2021 or thereafter, may be filed within the time provided in that section or by 31st August, 2021, whichever is later.

The Statement of Deduction of Tax for the last quarter of the Financial Year 2020-21, required to be furnished on or before 31st May, 2021 under Rule 31A of the Income-tax Rules,1962 (hereinafter referred to as “the Rules”), as extended to 30th June, 2021 vide Circular No.9 of 2021, may be furnished on or before 15th July, 2021.

The Certificate of Tax Deducted at Source in Form No.16, required to be furnished to the employee by 15th June, 2021 under Rule 31 of the Rules, as extended to 15th July, 2021 vide Circular No.9 of 2021, may be furnished on or before 31st July, 2021.

The Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64D for the Previous Year 2020-21, required to be furnished on or before 15th June, 2021 under Rule 12CB of the Rules, as extended to 30th June, 2021 vide Circular No.9 of 2021, may be furnished on or before 15th July, 2021.

The Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64C for the Previous Year 2020-21, required to be furnished on or before 30th June, 2021 under Rule 12CB of the Rules, as extended to 15th July, 2021 vide Circular No.9 of 2021, may be furnished on or before 31st July, 2021.

The application under Section 10(23C), 12AB, 35(1)(ii)/(iia)/(iii) and 80G of the Act in Form No. 10A/ Form No.10AB, for registration/ provisional registration/ intimation/ approval/ provisional approval of Trusts/ Institutions/ Research Associations etc., required to be made on or before 30th June, 2021, may be made on or before 31st August, 2021.

The compliances to be made by the taxpayers such as investment, deposit, payment, acquisition, purchase, construction or such other action, by whatever name called, for the purpose of claiming any exemption under the provisions contained in Section 54 to 54GB of the Act, for which the last date of such compliance falls between 1st April, 2021 to 29th September, 2021 (both days inclusive), may be completed on or before 30th September, 2021.

The Quarterly Statement in Form No. 15CC to be furnished by authorized dealer in respect of remittances made for the quarter ending on 30th June, 2021, required to be furnished on or before 15th July, 2021 under Rule 37 BB of the Rules, may be furnished on or before 31st July, 2021.

The Equalization Levy Statement in Form No. 1 for the Financial Year 2020-21, which is required to be filed on or before 30th June, 2021, may be furnished on or before 31st July, 2021.

The Annual Statement required to be furnished under sub-section (5) of section 9A of the Act by the eligible investment fund in Form No. 3CEK for the Financial Year 2020-21, which is required to be filed on or before 29th June, 2021, may be furnished on or before 31st July, 2021.

Uploading of the declarations received from recipients in Form No. 15G/15H during the quarter ending 30th June, 2021, which is required to be uploaded on or before 15th July, 2021, may be uploaded by 31st August,2021.

Exercising of option to withdraw pending application (filed before the erstwhile Income Tax Settlement Commission) under sub-section (1) of Section 245M of the Act in Form No. 34BB, which is required to be exercised on or before 27th June, 2021, may be exercised on or before 31st July, 2021.

Last date of linkage of Aadhaar with PAN under section 139AA of the Act, which was earlier extended to 30th June, 2021 is further extended to 30th September, 2021.

Last date of payment of amount under Vivad se Vishwas(without additional amount) which was earlier extended to 30th June, 2021 is further extended to 31st August, 2021.

Last date of payment of amount under Vivad se Vishwas (with additional amount) has been notified as 31st October, 2021.

Time Limit for passing assessment order which was earlier extended to 30th June, 2021 is further extended to 30th September, 2021.

Time Limit for passing penalty order which was earlier extended to 30th June, 2021 is further extended to 30th September, 2021.

Time Limit for processing Equalisation Levy returns which was earlier extended to 30th June, 2021 is further extended to 30th September, 2021.

The Indian Finance Budget for 2020 and 2021 has brought various amendments to TDS provisions to include the Assessees’ who were erstwhile not in the ambit of TDS and to collect TDS from non- income tax return filers at higher rates. This article will focus on the TDS sections that will be effect from July 01,2021 and the existing sections that will have different purview from July 01,2021.

Section 206AB – Resident

A tax deductor should ensure that from July 01,2021 TDS is deducted at:

twice the rate specified in the Act or

5%

Whichever is higher, if the person from whom the tax is deducted has:

Notfiled their income tax returns for immediately two preceding financial years, for which the due date has expired and

Aggregate TDS amount is equal to or more than INR 50,000 in each of the two previous years.

Section 206CCA – Resident

A tax collector should ensure that from July 01,2021 TCS is collected at:

twice the rate specified in the Act or

5%

Whichever is higher, if the person from whom the tax is collected has:

Not filed their income tax returns for immediately two preceding financial years, for which the due date has expired and

Aggregate TCS amount is equal to or more than INR 50,000 in each of the two previous years.

194Q – TDS on purchase of goods – Resident / Non resident

A tax deductor should ensure that from July 01,2021 TDS is deducted at 0.1% of amount paid to the person (including GST amount, unlike service invoices) if :

Payment is made towards purchase of goods and

If the turnover of the tax deductor is more than INR 10 crores in the previous year and

If the transaction between the tax deductor and the person from whom tax is deducted exceeds INR 50 Lakhs in a financial year (for this period, it will be considered from April 01, 2021, though it is applicable only from July 01, 2021)

Points to be Noted

The amount deductible as TDS is over and above the INR 50 Lakh rupees.

5% if there is no PAN/Aadhar with person to whom payment is made.

206 C (1H) – TCS On Sale Of Goods – Resident / Non Resident

A tax collector should ensure that from October 01,2020 TCS is deducted at 0.1% of amount received from the person (including GST amount, unlike service invoices) if :

Amount received is made towards sale of goods and

If the turnover of the tax collector is more than INR 10 crores in the previous year and

If the transaction between the tax collector and the person from whom tax is collected exceeds INR 50 Lakhs in a financial year (for this period, it will be considered from April 01, 2020, though it is applicable only from October 01, 2020)

Points to be Noted

5% if there is no PAN/Aadhar with person from whom amount is received.

Not Applicable if section 194Q is applicable to the buyer.

Not Applicable on imports and purchase by Central Govt or State Govt or Local Authority

The amount collectable as TCS is over and above the INR 50 Lakh rupees.

194 Q vs 206 C (1H) Case to Case Analysis

Buyers Turnover in PY

Sellers Turnover in PY

Transaction Value in CY

Applicability

5 Crore

15 Crore

60 Lakhs

206 C (1H)

15 Crore

5 Crore

60 Lakhs

194 Q

15 Crore

15 Crore

60 Lakhs

194 Q

5 Crore

5 Crore

40 Lakhs

Both not applicable

15 Crore

5 Crore

40 Lakhs

Both not applicable

5 Crore

15 Crore

40 Lakhs

Both not applicable

Overall Summary

Section

Applicability

Effective Date

Turnover

Transaction Limit

TDS / TCS Limit

ITR for preceding 2 FYs’

Rate

206 AB

OnlyResidents

July 01, 2021

NA

NA

> 50,000

Not Filed

NA

206CCA

OnlyResidents

July 01, 2021

NA

NA

> 50,000

Not Filed

NA

194 Q

Resident / Non-Resident

July 01, 2021

10 Crore

50 Lakhs

NA

NA

0.1%*

206 C (1H)

Resident / Non-Resident

October 01, 2020

10 Crore

50 Lakhs

NA

NA

0.1%*

*However, if an assessee fall under 206 AB or 206 CCA, their TDS and TCS rates will be 5%

How to Check Compliance of Vendor/Customer ?

Obtaining declaration from your Vendor/ Customer

The Assessee should prepare a format of declaration addressing to themselves from the Vendor/Customer in letter head of the customer. The format should be circulated to the Vendor/Customer and the same should be filled, signed, sealed and collected by the Assessee. The following points should form part of the declaration:

Whether the Vendor / Customer have filed their income tax returns for preceding two years

Whether their aggregate TDS/TCS is greater than 50,000 in previous year

To confirm if the turnover in PY is > 10 Crore, which decides applicability of 194Q/206C (1H) – If 194 Q is not applicable then 206 (1H) is applicable and vice versa, so it is advisable to get confirmation if the turnover of the assessee exceeds INR 10 Crore.

PAN of the Vendor/Customer

ITR Acknowledgement number for past two years

To verify from the new income tax portal

Circular No.11/2021 dated June 21, 2021 issued by CBDT, briefs about the functionality available for the tax deductors / collectors in the new Income Tax portal to check if the person from whom tax is deducted or collected has filed their income tax returns and if their aggregate TDS/TCS exceeds 50,000 with the help of their PAN, for compliance under Section 206AB and 206CCA. The site holds a list of specified persons who have not complied with conditions under 206AB and 206CCA.

In case of shortfall, interest payable at year end

Re-registration of Trust

Income Tax Act

30.06.2021

Not defined

Aadhar Pan Linking

Income Tax Act

30.06.2021

Not defined

Updation of IE Code

NDGFT

30.06.2021

Deactivation of Code

DPT -03

Companies Act, 2013

29.06.2021

INR 5000 + INR 500 per day

Q4 Results of Listed Companies

SEBI

30.06.2021

INR 5000 per day

GST Return for April and May 2021

Goods and Service Tax

Refer Below

Interest of 18% per annum and Late fee of 50-100 per day.

ESI Payment for the month of May

ESI Act

15.06.2021

12% p.a. on employer contribution + 5% Penalty

EPF Payment for the month of May

EPF Act

15.06.2021

12% p.a. on employer contribution + 5% Penalty

The above due dates do not ensure completeness of all due dates falling in the month of June 2021, however it is made as comprehensive as possible. It is advisable for the entities to check the applicability of respective acts and related compliances for which the due date fall in the month of June 2021.

TDS Payment for month of May

Taxpayers’ possessing valid TAN and deducted income taxes at source during the month of May should remit the same to the Government before Seventh of June. If not made before 7th, the same has to be paid along with interest of 1.5% per month calculated from date of deduction, which is 3% if paid anytime after 7th of June till 30th of June 2021.

Q4 TDS Return for FY 2020-21

The tax deductors who had deducted and remitted TDS for the period Jan-March 2021 should file their respective TDS returns i.e. 26Q, 24Q, 27Q etc., by end of June 30, 2021. The due date has been extended from its original due date of May 31, 2021. Non filing of TDS returns on time will result in penalty of INR 200 per day.

Re-registration of Trust/Institutions covered under Sec 12 AA, 80G and 10 (23C) of Income Tax Act.

The Budget 2020 introduced this process which got postponed due to the first wave of COVID in India. As on date, the due date to comply with this provision is June 30, 2021. The existing Trusts and Institutions covered under Sec 12AA, 80G and Sec 10 (23C) of Income tax should get themselves re-registered by filing form 10 A available in the Income tax portal by submitting the requisite documents as attachments to the form which includes the existing registration certificates, income tax returns/acknowledgements etc.,

This well-known compliance is applicable only to Individual Tax payers and it is happening over years with due dates extending forever, if you had filed income returns up to date, most likely your Aadhar is linked with your PAN, also if you have obtained PAN recently it is most likely that the PAN is linked with Aadhar. Still, it is advised to verify the linking if not done before, one should visit the new income tax portal to verify the same.

Notification 58/2015-20 of DGFT, has made the following provisions effective from 12th February 2021,

An IEC holder i.e. Import Export Code holder, has to ensure that details in IEC is updated electronically every year, during April-June period. In cases where there are no changes in IEC details same also needs to be confirmed online.

An IEC shall be de-activated, if it is not updated within the prescribed time. An IEC so de-activated may be activated, on its successful updation. This would however be without prejudice to any other action taken for violation of any other provisions of the FTP

An IEC may be also be flagged for scrutiny. IEC holders are required to ensure that risks flagged by the system is timely addressed; failing which the IEC shall be de-activated.

Filing of Form DPT-03

Companies other than government companies, banking and NBFCs are required to file Form DPT-03, if applicable, before June 29, 2021.

Applicability:

Every Company other than Government company, shall file a return of outstanding receipt of money or loan by a company but not considered as deposits, in terms of clause (c) of sub-rule 1 of rule 2 within 90 days from the closure of financial year i.e by 29th June.

Q4 Results of Listed Companies

The Listed companies should submit their Q4 results to SEBI on or before June 30, 2021, which is extended from its original due date of May 30, 2021. Not filing Q4 results by June 29, 2021 will result in penalty of INR 5,000 per day as per rule 33 of the Listing regulations.

GST Compliances

GSTR-1 Due Dates

Turnover

Period of return

Due Date

Monthly filers

May 2021

26.06.2021

QRMP Scheme

May 2021

28.06.2021

GSTR-3B Due Dates as per Amnesty Scheme

Failing to comply with above GST compliances will result in interest payment of 18% per annum on tax payable and late fee of INR 50-100 per day capped to INR 5,000 for CGST/SGST each and INR 10,000 /- for IGST per month. However late fee discounts and interest rebates are provided under GST Amnesty scheme.

In general, the Supplier of service/goods pays GST to the government on the supply made by him. This is called forward charge. In case of Reverse Charge Mechanism (“RCM”), the receiver of service/goods pays the GST amount directly to the government for the goods/ services received by him, instead of paying it to the supplier and then the supplier depositing. Such amount of tax deposited under reverse charge by receiver is eligible for input credit in the month subsequent to the month of payment of tax.

The liability to pay tax lies on the receiver in case of reverse charge. Even if the supplier of the service under reverse charge pays GST to the government, the liability of the receiver is not met. Such supplier who paid GST on RCM, can benefit out of it only by way of applying for refund and he cannot claim input on such tax paid. The receiver’s liability will still be considered as not discharged. Unlike Service tax, Reverse charge Mechanism does not have separate provisions in the GST Act. It is declared as a notified supply under Notification number 4/2017 – Central Tax rate in case of goods and Notification number 13/2017 – Central Tax rate in case of services, as amended from time to time.

Import of Service:

The import of services even for personal consumption would qualify as supply and therefore would be liable to tax. This would not be subject to the threshold limit for registration, as tax would be payable in case of import of services on reverse charge basis, requiring the importer of service to compulsorily obtain registration. However, the GST law has ensured that persons who are not engaged in any business activities will not be required to obtain registration and pay tax under reverse charge mechanism, and in turn, requires the supplier of services located outside India, to obtain registration for the OIDAR (Online information and database access and retrieval) services only.

Example: Mr. A is doing business and imports service for personal use, reverse charge mechanism will be applicable. Whereas Mr. B is a salaried individual and does no other business and imports service for personal use, then reverse charge mechanism is not applicable.

Import of Goods:

Customs act will govern the taxes on import of goods and accordingly IGST on import of goods will be paid by the importer. Key Points to be noted:

No partial reverse charge will be applicable under GST. 100% tax will be paid by the recipient if reverse charge mechanism applies.

All taxpayers required to pay tax under reverse charge have to mandatorily obtain registration and the threshold exemption is not applicable on them.

Payment of taxes under reverse charge cannot be made with utilisation of input tax credit and has to be made in cash

The recipient can take the credit of tax paid on inward supplies liable to reverse charge once the recipient makes payment of tax in cash.

When the supplier of the services covered under RCM is unregistered, the receiver of service is still liable to pay GST to the government.

The goods and services that are covered under reverse charge mechanism is listed below:

Goods covered under RCM in Notification number 4/2017, 36/2017 and 11/2018 – Central Tax rate

Tariff item, sub-heading, heading or Chapter

Description of supply of Goods

Supplier of goods

Recipient of supply

0801

Cashew nuts, not shelled or peeled

Agriculturist

Any registered person

1404 90 10

Bidi wrapper leaves (tendu)

Agriculturist

Any registered person

2401

Tobacco leaves

Agriculturist

Any registered person

5004 to 5006

Silk yarn

Any person who manufactures silk yarn from raw silk or silk worm cocoons for supply of silk yarn

Any registered person

Supply of lottery

State Government, Union Territory or any local authority

Lottery distributor or selling agent. Explanation.- For the purposes of this entry, lottery distributor or selling agent has the same meaning as assigned to it in clause (c) of Rule 2 of the Lotteries (Regulation) Rules, 2010, made under theprovisions of sub section 1 of section 11 of the Lotteries (Regulations) Act, 1998 (17 of 1998).

Any Chapter

Used vehicles, seized and confiscated goods, old and used goods, waste and scrap

Central Government, State Government, Union territory or a local authority

Any registered person

Any Chapter

Priority Sector Lending Certificate

Any registered person

Any registered person

Services covered under RCM in Notification number 10/2017 Integrated tax rate and 13/2017, 33/2017, 29/2018 and 22/2019 – Central Tax rate Items coloured in yellow are there in both Central tax rate and Integrated tax rate. Items in bold are recent amendments applicable from 01 October 2019.

Category of Supplier of Services

Supplier of Service

Recipient of Service

Any service supplied by any person who is located in a non taxable territory to any person other than non taxable online recipient

Any person located in a non taxable territory

Any person located in the taxable territory other than non taxable online recipient.

Supply of Services by a goods transport agency (GTA) in respect of transportation of goods by road to- (a) any factory registered under or governed by the Factories Act, 1948(63 of 1948);or (b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person

Goods Transport Agency (GTA)

(a) Any factory registered under or governed by the Factories Act, 1948(63 of 1948); or (b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or theState Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person; located in the taxable territory

Services supplied by an individual advocate including a senior advocate by way of representational services before any court, tribunal or authority, directly or indirectly, to any business entity located in the taxable territory, including where contract for provision of such service has been entered through another advocate or a firm of advocates, or by a firm of advocates, by way of legal services, to a business entity.

An individual advocate including a senior advocate or firm of advocates.

Any business entity located in the taxable territory.

Services supplied by an arbitral tribunal to a business entity.

An arbitral tribunal.

Any business entity located in the taxable territory.

Services provided by way of sponsorship to any body corporate or partnership firm.

Any person

Any body corporate or partnership firm located in the taxable territory.

Services supplied by the Central Government, State Government, Union territory or local authority to a business entity excluding, – (1) renting of immovable property, and (2) services specified below- (i) services by the Department of Posts by way of speed post, express parcel post, life insurance, and agency services provided to a person other than Central Government, State Government or Union territory or local authority; (ii) services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport; (iii) transport of goods or passengers.

Central Government, State Government, Union territory or local authority

Any business entity located in the taxable territory.

Services supplied by a director of a company or a body corporate to the said company or the body corporate.

A director of a company or a body corporate

The company or a body corporate located in the taxable territory.

Services supplied by an insurance agent to any person carrying on insurance business.

An insurance agent

Any person carrying on insurance business, located in the taxable territory

Services supplied by a recovery agent to a banking company or a financial institution or a nonbanking financial company.

A recovery agent

A banking company or a financial institution or a non-banking financial company, located in the taxable territory.

Services supplied by a person located in non- taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India.

A person located in nontaxable territory

Importer, as defined in clause (26) of section 2 of the Customs Act, 1962(52 of 1962), located in the taxable territory.

Supply of services by a music composer, photographer, artist or the like by way of transfer or permitting the use or enjoyment of a copyright covered under clause (a) of sub-section (1) of section 13 of the Copyright Act, 1957 relating to original dramatic, musical or artistic works to a music company, producer or the like.

Music composer, photographer, artist, or the like

Music company, producer or the like, located in the taxable territory

Supply of services by an author by way of transfer or permitting the use or enjoyment of a copyright covered under clause (a) of sub-section (1) of section 13 of the Copyright Act, 1957 relating to original literary works to a publisher.

Author

Publisher located in the taxable territory: Provided that nothing contained in this entry shall apply where, –(i) the author has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017), and filed a declaration, in the form at Annexure I, within the time limit prescribed therein, with the jurisdictional CGST or SGST commissioner, as the case may be, that he exercises the option to pay central tax on the service specified in column (2), under forward charge in accordance with Section 9 (1) of the Central Goods and Service Tax Act, 2017 under forward charge, and to comply with all the provisions of Central Goods and Service Tax Act, 2017 (12 of 2017) as they apply to a person liable for paying the tax in relation to the supply of any goods or services or both and that he shall not withdraw the said option within a period of 1 year from the date of exercising such option;(ii) the author makes a declaration, as prescribed in Annexure II on the invoice issued by him in Form GST Inv-I to the publisher

Supply of services by the members of Overseeing Committee to Reserve Bank of India

Members of Overseeing Committee constituted by the Reserve Bank of India

Reserve Bank of India

Services supplied by individual Direct Selling Agents (DSAs) other than a body corporate, partnership or limited liability partnership firm to bank or non-banking financial company (NBFCs).

Individual Direct Selling Agents (DSAs) other than a body corporate, partnership or limited liability partnership firm.

A banking company or a non-banking financial company, located in the taxable territory

Services provided by business facilitator (BF) to a banking company

Business facilitator (BF)

A banking company, located in the taxable territory

Services provided by an agent of business correspondent (BC) to business correspondent (BC).

An agent of business correspondent (BC)

A business correspondent, located in the taxable territory

Security services (services provided by way of supply of security personnel) provided to a registered person: Provided that nothing contained in this entry shall apply to, – (i)(a) a Department or Establishment of the Central Government or State Government or Union territory; or (b) local authority; or (c) Governmental agencies; which has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017) only for the purpose of deducting tax under section 51 of the said Act and not for making a taxable supply of goods or services; or (ii) a registered person paying tax under section 10 of the said Act.

Any person other than a body corporate

A registered person, located in the taxable territory.

Services provided by way of renting of a motor vehicle provided to a body corporate.

Any person other than a body corporate, paying central tax at the rate of 2.5% on renting of motor vehicles with input tax credit only of input service in the same line of business

Any body corporate located in the taxable territory.

Services of lending of securities under Securities Lending Scheme, 1997 (“Scheme”) of Securities and Exchange Board of India (“SEBI”), as amended.

Lender i.e. a person who deposits the securities registered in his name or in the name of any other person duly authorised on his behalf with an approved intermediary for the purpose of lending under the Scheme of SEBI

Borrower i.e. a person who borrows the securities under the Scheme through an approved intermediary of SEBI.”.

The recent amendment in the reverse charge mechanism that will be applicable to most of the corporates include services received by a body corporate from a rent a cab service provider who are not corporates but charges GST at the rate of 5% and takes ITC only on similar line of business. This amendment is coming into effect from 01 October 2019. Refer Notification no.22/2019, Central Tax (Rate) for amendments with effect from 01 October 2019.

Whenever an Individual is preparing his income tax return, he/she in general tend to forget there are Income heads other than Salaries. The most common income not included in the income tax of the individuals would be interest earned from savings bank account and interest from fixed deposits. The interest from savings account is eligible for deduction under Section 80TTA up to INR 10,000. The interest from fixed deposit earned by senior citizens is eligible for deduction under section 80 TTB up to INR 50,000.

In addition to the interest income, the individuals should also consider gifts if any obtained by them, while filing their income tax returns. The gifts need not necessarily be claimed as gift. When a husband transfers an amount to his wife for any reason and when source of such amount is not included in his income tax return, then such amount is deemed to be a gift in the hands of his wife. Such transfer can be cash, immovable property or any other property. Let us see the taxability of such transfers in detail.

Taxability of Gifts

a) Gift in the form of CASH When any person receives cash from another a sum of value more than INR 50,000 without consideration (i.e. gift), the entire sum received will be taxable in the hands of the receiver. If the sum received is INR 50,000 or less the sum received will not be taxable in the hands of the receiver. Example: If Mr. Z gifts Mr. X INR 55,000, MR. Y INR 48,000 and Mr. W INR 50,000 in the form of cash, it Is taxable only for Mr. X and it is not taxable for Mr. Y and W.

b) Gift in the form Immovable Property (Land) With Zero Consideration When any person receives any immovable property from another without consideration and the stamp duty value of such immovable property received is more than INR 50,000, then the stamp duty value of such immovable property is taxable. If the stamp duty value of such property received is less than INR 50,000 then it is not taxable. With Consideration less than stamp duty value When any person receives an immovable property from another with a consideration(sale value) less than the stamp duty valueof such immovable property, the amount of difference between stamp duty value and the consideration is taxable only if it is more than higher of the two mentioned below: a) Amount of fifty thousand rupees and b) Amount equal to 5 percent of the consideration

Example: 1. Mr. A gifts Mr. B an immovable property with stamp duty value INR 40,000 and gifts another immovable property worth INR 60,000 to Mr. C As the stamp duty value is less than INR 50,000 it is not taxable for B and it is fully taxable for Mr. C as the stamp duty value is greater than INR 50,000.

2 . Mr. D pays Mr. A INR 20,000 for an immovable property with stamp duty value INR 70,000 and Mr. E pays Mr. A INR 30,000 for an immovable property with stamp duty value of INR 90,000. Considering the excess of stamp duty value not paid by Mr. D and Mr. E, for Mr. D the excess value did not exceed INR 50,000 and hence it is not taxable and for Mr. E it is taxable as the difference between stamp duty value and the consideration is in excess of INR 50,000 (considering higher of INR 50,000 and 5% of 20,000 (1000) in case of Mr. D and 5% of 30,000 (1500) in case of Mr. E

c) Gift in the form other than cash and immovable property When a person receives gift other than cash and immovable property and if the value of such gift (property without consideration) exceeds INR 50,000 then the same will be taxable in the hands of receiver. When a person receives gift other than cash and immovable property for a consideration which is less than the fair market value of such property and if such amount exceeding consideration is more than INR 50,000 then such sum exceeding consideration will be taxable in the hands of receiver. Example: a) Miss G gifts Ms. F jewellery worth INR 20,000 b) Miss G gifts Ms. H jewellery worth INR 1,00,000 for INR 40,000 Jewellery received by Ms. F is not taxable and jewellery received by Ms. H is taxable to the extent of INR 60,000. Exemption: The above provisions are not applicable when a person receives such cash or property: a) From any relative – relative in relation to an individual means the husband, wife, brother or sister or any lineal ascendant or descendent of that individual. b) On the occasion of the marriage of an individual c) Under a will or by way of inheritance d) In contemplation of death of the payer or donor as the case may be e) From any local authority f) From any fund or foundation or university or other educational institution or hospital or other medical institution or any trust or institution or any other funds of the central or state government g) From or by any trust or institution registered under Income tax Act h) Any compensation or other payment, due to or received by any person, by whatever name called, in connection with the termination of his employment or the modification of the terms and conditions relating thereto.